Trump Accounts and 529 Plans

![]()

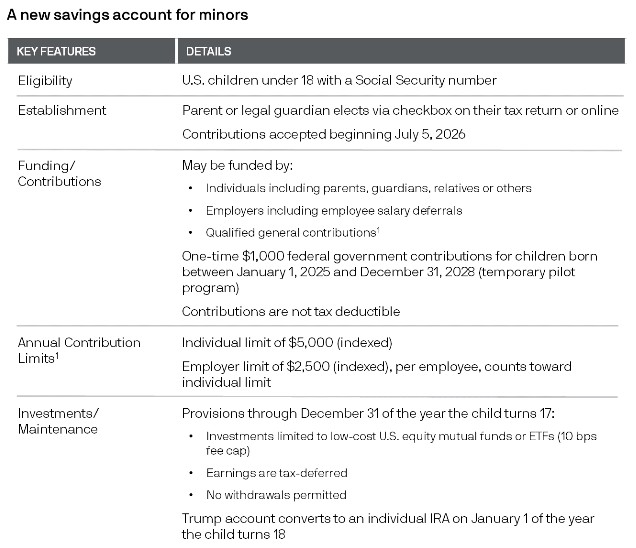

Trump Accounts

Starting July 5, 2026 family, friends, charities and employers may contribute up to $5,000 to each Trump account each year until the child turns 18. A Trump Account can be opened for any U.S. citizens child under the age of 18 who has a valid social security number with a legal guardian, parent, adult sibling, or grandparent (in that order) establishing the account. You cannot contribute until the program launches on July 4th, but you can sign up for a Trump account at trumpaccounts.gov or by filing Form 4547. There is no automatic enrollment. Additionally, every child born between January 1, 2025, and December 31, 2028, is eligible to receive a one-time $1,000 contribution from the Treasury Department.

Trump accounts function similar to a Traditional IRA. Earnings grow tax-deferred and withdrawals will be taxed at ordinary income rates. No distributions are permitted until the child turns 18. Trump accounts convert to an individual IRA on January 1 of the year the child turns 18. Funds can be accessed without penalty when the child turns 18 for qualified expenses like education, a first-time home purchase, or starting a business. Otherwise, withdrawals before age 59 ½ would be subject to a 10% penalty just like an IRA.

Additional guidance regarding contributions, investments, distributions, special rules, etc. is expected in the second half of 2026.

The real power of the Trump Account: Roth conversions

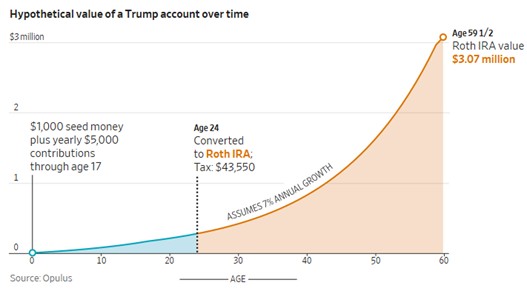

At age 18 when this account essentially becomes an IRA, it is subject to the same 10% penalty for most withdrawals, taxed at ordinary income rates, and RMD’s start at age 75. However, these accounts can be converted to a Roth IRA. According to a recent Wall Street Journal article, “The Hack That Turns Trump Accounts Into Multimillion-Dollar Tax-Free Nest Eggs,” parents can potentially build multimillion-dollar tax-free retirement accounts for children by combining early contributions with strategic Roth conversions. An ideal time to complete the conversion is after the “Kiddie Tax” rule and during the child’s potentially low-income years in their 20s. The Kiddie Tax can apply to unearned income for certain children under 24, including full-time students 19-23 that do not provide more than half of their own support. The child would owe the tax on the Roth conversion, but the key is the tax would be owed at their likely lower tax rate and not the parents. Parents could also pay the tax on the conversion as an additional gift.

The below illustration outlines the power of this strategy by taking advantage of the $1,000 seed money, contributing $5,000 a year until age 18 and then converting to a Roth at age 24. Assuming a median-income young worker, with wages and federal tax brackets adjusted for inflation, the tax due on a 24-year-old’s conversion of a $278,047 balance would be $43,550, paid for by parents or grandparents. That would lead to a tax-free Roth of just over $3 million at 59½.

529 Accounts: Still the gold standard for education funding

The creation of Trump accounts provides a new interesting strategy to consider for helping fund your children’s retirement. Furthermore, if you have a child that is eligible for the $1,000 seed money it does not hurt to at the very least take the government contribution.

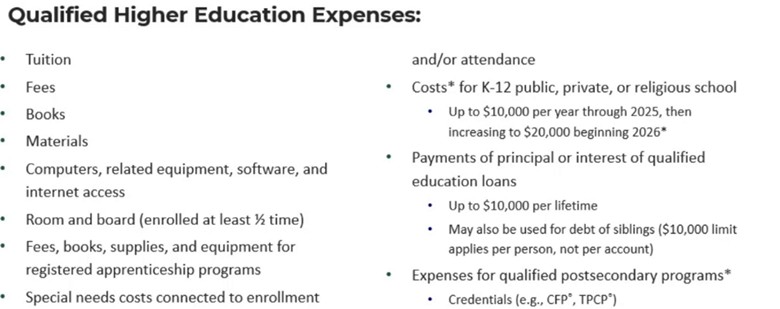

However, we recommend setting aside funds in a 529 account first. The $5,000 contribution limit is likely not going to cover expenses for a high-level college and there is no tax break on the earnings since it will come out as ordinary income. Compared to a 529 where earnings grow tax deferred and are tax free for qualified education withdrawals. There are also no contribution limits until the account hits the state’s maximum account balance, typically around $500,000. Another unique feature is the ability to superfund 5 years’ worth of the annual gift tax exclusion in one year. 529’s also allow the ability to change the beneficiary to eligible family members if the funds are not being used. They continue to expand what is included as a qualified expense including postsecondary designations and increasing the limit from $10,000 to $20,000 for K-12 expenses.

So while funding Trump accounts is something to consider, 529’s are still considered the gold standard for education funding.

“Trump Accounts: Legislative and Regulatory Considerations.” J.P. Morgan Asset Management, 2026.

“College Planning Essentials.” J.P. Morgan Asset Management, 2026.