Roth Opportunities for Teens and Young Adults

Roth: How and How Much to Contribute

A Roth IRA offers tax-free growth, making it a very attractive vehicle for young investors to take advantage of decades of compounding. If a child has earned income (reported on a tax return) from a summer job or other work, a full or partial Roth contribution may be an option. Earned income does not include interest or dividends.

A child must have earned income, but he or she does not have to personally contribute the money to the Roth; a parent (or anyone else) can fund the Roth IRA as a gift. Just remember, they cannot save more in a Roth than they earned. So if they work a summer job and made only $3,000, the most they (or you) could contribute to their Roth would be $3,000.

Accounts for minors are usually established with an adult custodian to oversee the account until the child is 18 or 21. Any money contributed to the kids’ Roth IRA by someone else is considered a gift. This may be accomplished without any income tax or estate tax complications through use of the annual gift-tax exclusion.

The current limit for 2017 tax-year Roth contribution is $5,500 a year for an individual under the age of 50. One must also have adjusted gross income below certain levels to make Roth contributions, which generally won’t restrict young savers (for the 2017 tax-year, the phase out begins at $118,000 and ineligibility begins at $133,000). The deadline for a 2017 tax-year contribution is April 18, 2018.

The Value of a Roth

When a young adult is just starting to invest, the Roth should be their first stop --- even before they open a taxable account, or contribute to a workplace retirement-savings plan. There are exceptions; if their employer offers a match on their 401(K) contributions, or if they are able to make Roth contributions to their 401(K). A match is free money that should not be passed up, and the young adult should consider contributing enough to win the match, then send any additional money to the Roth IRA. (Yes, they can invest in both a Roth and a workplace retirement plan.)

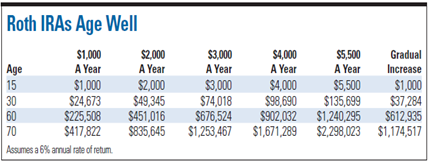

For those just starting out, the power of this tax shelter may seem a tad obscure, but it can really pay off big. If a 25-year-old contributes $5,500 each year until she retires and makes an average return of 8% on her investment, she’ll have $1.7 million saved by the time she is 65. And the money is all hers – she won’t have to give the IRS a cent of it if she waits until retirement to withdraw the earnings.

Withdrawing From Your Roth

Roth IRA owners may withdraw contributions at any time without taxes or penalties. Earnings growth above contributions may be taxable and subject to a 10% penalty if withdrawn before 59 ½. There is no mandatory withdrawal age, meaning assets can continue to grow tax-free even well into retirement. Upon death, a Roth IRA can pass income tax-free to heirs. Non-spouse heirs must take distributions based on their life expectancies set by the IRA but the required distributions are generally tax-free.

Young adults may tap their Roth to buy their first home. As noted, you can always withdraw contributions tax-and penalty-free for any purpose. If using contributions for a first-home purchase, an individual can withdraw up to $10,000 of earnings tax- and penalty-free if the account has been open for at least five years. If the account is less than five years young, the withdrawal will still be penalty-free, but a tax will be incurred on the withdrawn earnings. That $10,000 limit is per person, so couples could withdraw up to $20,000 of earnings if they each have a Roth.

However, let us not let the withdrawal conversation to get us too far ahead of ourselves. For now, we will stress the importance of encouraging your child to open a Roth as soon as they have earned, reportable income.

If you have any questions, or would like to consider a Roth IRA for you or your child, please contact us at 617-622-1500.

Sources: Fidelity, IRS, Sandy Cove Advisors, Vanguard