Key 529 Plan Updates from the OBBBA (Effective July 4, 2025)

The good news is that each new tax bill continues to bring greater flexibility and enhancements to 529 plans. Recent legislative changes have expanded the definition of qualified education expenses. Offering families more options for how they use these tax-advantages accounts. For elementary and secondary education, eligible expenses now include not only tuition, but also curriculum and instructional materials (such as books or online courses), tutoring by licensed or expert instructors, dual‑enrollment fees, standardized test (e.g. SAT/ACT) fees, and educational therapies for students with disabilities. These changes make 529 plans more versatile than ever for meeting a wide range of educational needs.

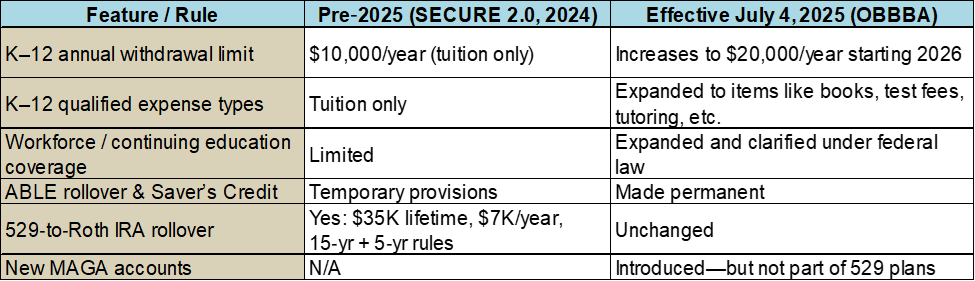

Here’s a clear and up‑to‑date summary of the changes to 529 plans under the “One Big Beautiful Bill Act” (OBBBA) that took effect on or after July 4, 2025:

1. K–12 Withdrawal Limit Doubled to $20,000

Starting in 2026, families can withdraw up to $20,000 per year from 529 plans for qualified K‑12 expenses—up from $10,000 annually. Qualified expenses include not only tuition but expanded items like books, standardized test fees, curriculum materials, tutoring, and online education resources.

2. Broader Definition of K–12 Qualified Expenses

Earlier the bill also expanded qualified K‑12 expenses to include non‑tuition items (books, exam costs, homeschooling resources, educational therapy, etc.)—without extra federal tax. States may need to enact conforming laws to allow such deductions at the state level.

3. Workforce Training & Continuing Education Coverage Expanded

Funds may now be used tax‑free for training registered under the Workforce Innovation and Opportunity Act, covering tuition, fees, books, supplies, and exam fees in career training and continuing education.

4. 529‑to‑Roth IRA Rollovers (unchanged)

- Beneficiaries can roll over up to $35,000 lifetime from a 529 plan into their own Roth IRA (via trustee‑to‑trustee rollover)

- Must meet the following:

- 529 account held for at least 15 years

- Funds contributed or earned in the last 5 years excluded

- Annual Roth IRA contribution limits apply (2025: $7,000 per year—or $8,000 if age 50+)

- Beneficiaries must have earned income at least equal to the rollover amount

- Roth IRA income limits do not apply for these rollovers

- Apprenticeships & Student Loan Payments

5. ABLE‑Account Provisions Made Permanent

An ABLE account (Achieving a Better Life Experience) is a tax-advantaged savings account for individuals with disabilities. It allows people with disabilities and their families to save and invest money for disability-related expenses without losing eligibility for government benefits like SSI (Supplemental Security Income) and Medicaid.

Certain ABLE features had been set to expire at the end of 2025; OBBBA now makes them permanent:

- 529‑to‑ABLE rollovers-you can roll over funds from a 529 plan into an ABLE account for the same beneficiary or a family member of that beneficiary. These rollovers are subject to the annual ABLE account contribution limit.

- ABLE‑to‑Work contributions The “ABLE to WORK” provision, passed as part of the Tax Cuts and Jobs Act of 2017, allows certain ABLE account owners who work and earn income to contribute above the annual ABLE contribution limit. To be eligible, the ABLE account holder, or their employer, cannot contribute into a defined contribution plan such as 401(a), 403(a) or 401(k) plan; an annuity such as a 403(b) contract; or an eligible, deferred compensation plan, such as a Section 457(b) plan in the calendar year.

- Saver’s Credit for ABLE contributions The Saver's Credit is a tax credit designed to encourage low and moderate-income individuals to save for retirement or to an ABLE account.

6. MAGA “Kids” Accounts Start in 2026 (Not Part of 529 Plans)

The bill creates new MAGA (Money Accounts for Growth and Advancement) savings accounts (distinct from 529s):

- Open to U.S. children born between January 1, 2025 and January 1, 2029

- Eligible families receive a one‑time $1,000 federal seed deposit

- Annual individual contributions up to $5,000 (tax‑deferred growth)

- Taxed at long‑term capital gains rates if used for education, first‑home purchase, or small business startup; withdrawals for any purpose allowed after age 30

7. Gift Tax & Front‑Loading Limits (2025)

- Annual federal gift tax exclusion is $19,000 per person, or $38,000 per married couple

- Contributions to 529 plans are considered gifts for this purpose—and may be front‑loaded up to 5 years at once per beneficiary ($95,000 if single or $190,000 if married filing jointly) without triggering gift tax.

These updates allow families to use 529 funds for a wider range of educational and career-related needs—making 529 plans even more powerful tools for lifelong learning and savings.