You Have Inherited an IRA, Now What?

Losing a loved one is never easy, and inheriting an IRA often adds another layer of complexity during an already difficult time. The financial decisions surrounding an inherited IRA are frequently time-sensitive and can have significant long-term tax implications. While it may seem like a windfall, you need to factor in the tax implications. Understanding the rules and available options is essential to making informed decisions and avoiding costly mistakes. Since 2020, a law known as the SECURE Act has changed the rules significantly. This guide walks through what you need to know Post-Secure Act (death of an owner on or after January 1, 2020) in three simple steps.

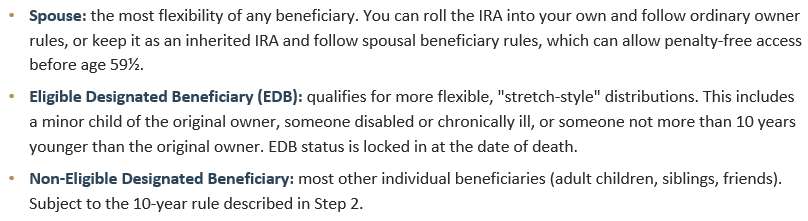

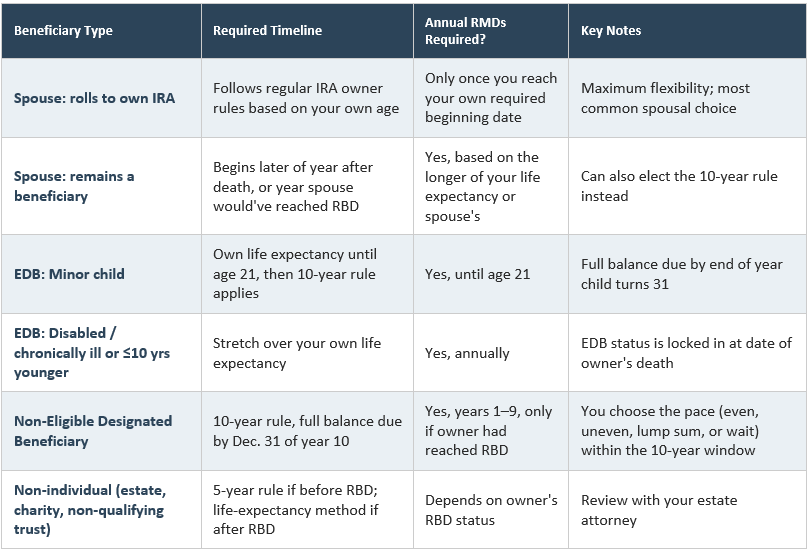

Your relationship to the person who passed away, plus a few personal circumstances, determines which rules apply. Beneficiaries generally fall into one of three groups:

The 10-Year Rule (Non-Eligible Designated Beneficiaries)

The entire inherited account must generally be emptied by December 31 of the 10th year after the original owner's death. Within that window, you can:

- Withdraw it all at once (simplest, but often most expensive at tax time)

- Spread withdrawals evenly across the 10 years

- Spread withdrawals unevenly, taking more in lower-income years and less in higher-income years

- Wait until year 10 to take a single distribution

Does the 10-Year Rule Also Require Annual RMDs?

This depends on the original owner's age, not yours. If the original owner had already reached their required beginning date (RBD), currently age 73 for those born 1951–1959, or 75 for 1960 and later, you must also take annual RMDs in years one through nine. If they had not yet reached their RBD, no annual RMDs are required; you simply need the account empty by year 10.

Other Situations at a Glance:

- Eligible Designated Beneficiaries (other than minor children): can stretch distributions over their own life expectancy instead of the 10-year rule.

- Minor children: take life-expectancy-based distributions until age 21, then the 10-year rule applies; the account must be fully distributed by the year the child turns 31.

- Spouses who remain beneficiaries: begin distributions the later of the year after death or the year the spouse would have reached their RBD, using the longer life expectancy of the two, or may elect the 10-year rule.

At a Glance: Options by Beneficiary Type

Distributions from an inherited traditional IRA are taxed as ordinary income in the year you take them. The timing is not just administrative, spreading withdrawals to manage tax brackets, and weighing continued tax-deferred growth against a large future tax bill, are core parts of the right strategy for you.

- Confirm your beneficiary type. It determines which rules apply to you.

- Know your deadline. Mark it so you are not caught off guard.

- Build a withdrawal strategy, not just a compliance plan. Timing can meaningfully affect your lifetime tax bill.

- Review your own beneficiary designations. A good moment to make sure your accounts reflect your wishes.

- Talk with us before you act. We can help coordinate the decision with your broader financial picture.