Roth Catch up Contributions - Key Changes Ahead

Key Changes Ahead: Roth Catch-up Contributions

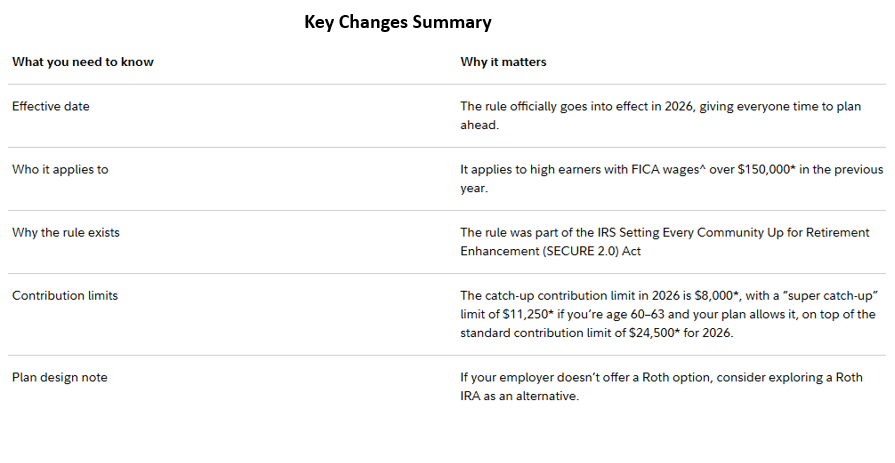

Starting in 2026, high earners age 50 and older must make catch-up contributions to an employer plan (401k, 403b, 457(b), etc.) as Roth contributions (after-tax contributions). High earners are defined as participants who earn in excess of $150,000 in FICA wages (indexed annually) the previous year, starting with 2025 wages.

The catch-up portion of $8,000 or $11,250 for ages 60-63 must now be made as Roth contributions. However, there is no change to the standard contribution limits pre-tax eligibility and the 2026 contribution limit to an employee plan is $24,500. Additionally, this change does not apply to catch-up contributions to an IRA.

With a Roth contribution, you pay taxes when you make contributions, but when you take a qualified distribution, you will not owe taxes on that money or any growth (as long as you are 59 ½ and have held the account for at least 5 years). Alternatively, the pre-tax contributions go into your account without being taxed, which can lower your taxable income now, but you will pay taxes when you eventually take it out.

Employers will need to update plans to allow for Roth 401k deferrals. If your plan does not allow this, you will be unable to make catch up contributions. Since it is expected that more employers will be updating their plans to allow for Roth 401k deferrals, it is important to be aware of this change even if the new requirement does not apply to you today. You may consider making a portion or all your $24,500 annual contribution to the Roth 401k, given the flexibility Roth’s allow due to their tax-free withdrawals.

Next steps:

Check your employer plan to make sure the Roth 401k deferral option is available in your plan

- If 50 or older in 2026 and making more than $150,000 in 2025 FICA wages, change your catch-up contributions to Roth

- If this change doesn’t apply to you, consider allocating a portion of the annual contribution limit to a Roth 401k for flexible retirement income