Introduction to the One Big Beautiful Bill Act

The "One Big Beautiful Bill Act" (OBBBA or OBBB) is a significant piece of U.S. federal legislation, signed into law by President Donald Trump on July 4, 2025. The OBBBA is designed to provide substantial tax cuts, primarily by making permanent many provisions of the 2017 Tax Cuts and Jobs Act (TCJA) that were set to expire at the end of 2025. Passed through budget reconciliation, allowing for a simple majority vote in the Senate, this act represents a sweeping overhaul of tax and spending policies, aiming to align with the Trump administration's second-term priorities. While hailed by proponents as a boon for the economy and American families, critics raise serious concerns about its impact on the national debt and social safety nets.

The OBBBA introduces several key changes intended to stimulate economic growth and provide financial relief to various segments of the population:

Individual Tax Relief and Adjustments

A cornerstone of the OBBBA is the permanent extension of the individual income tax rates established by the 2017 TCJA, with a top rate of 37% and a bottom rate of 10%. This prevents a widespread tax increase that would have otherwise occurred. The standard deduction amounts are also made permanent and increased for 2025 (e.g., to $15,750 for single filers and $31,500 for joint filers), with inflation indexing thereafter.

The act also provides several targeted tax deductions and credits:

- Child Tax Credit (CTC): The maximum CTC increases from $2,000 to $2,200 per child starting in tax year 2025 and is indexed for inflation. To qualify, both the parent(s) and child must have a Social Security number.

- Senior Bonus Deduction: A temporary (2025-2028) additional deduction of $6,000 for seniors (age 65+) is introduced, phasing out at higher income levels ($75,000 for single filers, $150,000 for joint filers). This aims to offset taxes on Social Security benefits for many retirees.

- Deductible Car Loan Interest: Buyers of U.S.-assembled vehicles can deduct up to $10,000 annually in auto loan interest through 2028, subject to income limitations, promoting domestic manufacturing.

- Mortgage Interest Deduction: The existing limit of $750,000 in mortgage debt ($375,000 for single filers) for the mortgage interest deduction is made permanent. Mortgage insurance premiums will also qualify for deduction.

- No Tax on Overtime and Tips: Temporary deductions (2025-2028) are introduced for qualified overtime compensation (up to $12,500 for single filers, $25,000 for joint filers) and up to $25,000 in qualified tip income. These deductions phase out for incomes above $150,000 for single filers and $300,000 for joint filers.

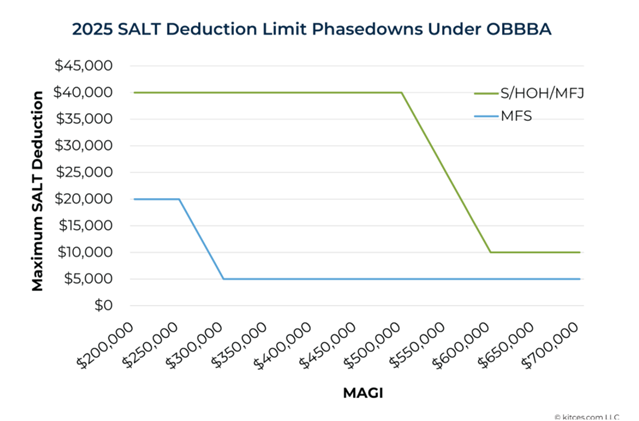

- SALT Deduction Increase: The cap on the State and Local Tax (SALT) deduction for itemizers is temporarily raised from $10,000 to $40,000 ($20,000 for married filing separately) for taxpayers below certain income thresholds, providing relief for residents in high-tax states. This cap adjusts for inflation and phases down by 30% for incomes above $500,000 ($250,000 for married filing separately), eventually reverting to $10,000 in 2030. The bill does not limit SALT deductions for pass-through entities.

- Charitable Deductions: For non-itemizers, a permanent above-the-line charitable deduction of up to $1,000 ($2,000 for joint filers) for cash contributions is reinstated starting 2026. For itemizers, a new floor of 0.5% of AGI is introduced for charitable deductions, meaning contributions are deductible only to the extent they exceed 0.5% of AGI. The deduction for those in the highest 37% tax bracket is capped at 35% of donated dollars.

- Repeal of Personal Exemptions: The personal exemption deduction is permanently eliminated, a change initially made by the TCJA.

- Alternative Minimum Tax (AMT): Changes made by the TCJA, including increased AMT exemptions and higher income thresholds for phase-out, are made permanent, though the phase-out rate for the exemption is increased at certain income thresholds.

Business Investment and Growth Incentives

The OBBBA includes provisions aimed at encouraging business investment and growth:

- 100% Bonus Depreciation: The act reinstates and allows for 100% first-year bonus depreciation for qualified property acquired on or after January 20, 2025, and placed in service before January 1, 2031. It also introduces an elective 100% deduction for qualified production property used in U.S. manufacturing. This is expected to accelerate write-offs and free up capital for reinvestment.

- Section 179 Expensing: The Section 179 deduction limit for small businesses has significantly increased from $1 million to $2.5 million, with the phase-out threshold beginning at $4 million. This change allows small businesses to deduct the full purchase price of qualifying equipment and/or software purchased or financed during the tax year, rather than depreciating it over several years—enabling faster cost recovery and encouraging investment.

- R&D Expensing: The legislation provides for immediate expensing of domestic R&D expenses, while foreign R&D must still be amortized over 15 years.

- Qualified Business Income (QBI) Deduction: The 20% deduction for QBI (Section 199A) for pass-through entities like sole proprietorships, partnerships, and S corporations is made permanent. A new minimum deduction of $400 for taxpayers with at least $1,000 of pass-through income begins in 2026.

- Qualified Small Business Stock (QSBS): Key changes to Section 1202 benefits include shortening the holding period to 3 years from 5 for a phased gain exclusion (50% in year 3, 75% in year 4, 100% after year 5), increasing the capital gain exclusion to $15 million from $10 million, and raising the gross asset limit to $75 million from $50 million.

- 1099 Information Reporting: The reporting threshold for payments to independent contractors and for miscellaneous income increases from $600 to $2,000 for payments made after December 31, 2025.

Other Notable Provisions

- "Trump Accounts": Starting 2026, these new savings accounts for U.S. citizen children under 18 allow contributions of up to $5,000 annually (indexed for inflation), treated similarly to non-deductible Traditional IRAs. Children born between January 1, 2025, and December 31, 2028, qualify for an initial $1,000 federal seed money.

- Expanded HSAs and 529s: The bill widens eligibility for Health Savings Accounts (HSAs) and allows payments for direct primary care arrangements and makes permanent telehealth extensions. 529 funds can now be used for testing fees, tutoring outside the home, educational therapies for students with disabilities, and tax-free withdrawals for recognized postsecondary credential programs.

- College and University Endowment Tax: A new multi-tiered endowment tax rate structure is created for schools with at least 3,000 tuition-paying students, based on their "student adjusted endowment." New reporting requirements are also included.

- Executive Compensation Excise Tax: The excise tax on compensation over $1 million paid by certain tax-exempt organizations is expanded to include all current and former employees, not just the top five most highly compensated.

- Tax Credit for Scholarship Granting Organizations (SGOs): A new tax credit (up to $1,700 per year) is created for contributions to SGOs that provide K-12 and college scholarships, offering a direct dollar-for-dollar reduction of federal income tax liability.

- Debt Ceiling Increase: The bill raises the U.S. debt ceiling by $5 trillion, preventing a potential government default.

- Defense Spending: An additional $150 billion in defense spending is allocated, including funds for shipbuilding. Funding is also provided for air traffic control, NASA, and agricultural safety net programs.

Conclusion

The One Big Beautiful Bill Act is a landmark piece of legislation with far-reaching implications for the U.S. economy, individual taxpayers, and social programs. It largely solidifies the tax regime established by the 2017 TCJA while introducing new deductions and incentives aimed at stimulating specific economic activities and providing targeted relief. However, its significant cuts to social safety nets and projected contribution to the national debt have ignited fierce opposition and underscore a fundamental philosophical divide on the role of government and economic priorities. As the provisions of the OBBBA are implemented and its effects unfold, its long-term impact on economic growth, income distribution, and the well-being of American citizens will continue to be a subject of intense scrutiny and ongoing debate.