Intrafamily Loans in 2026

With conventional mortgage rates still elevated compared to the near-zero levels of a few years ago, combined with the sharp increase in home prices, affording a home has become increasingly challenging. Loans among family members, "intrafamily loans," remain a popular way to help family members finance the purchase of a home on better terms, and to keep interest payments circulating within the family instead of going to a bank.

The basic principle of an intra-family loan is fairly straightforward, rather than borrowing money from a bank, a family member in need borrows money from someone else in the family, such as a child borrowing money from his/her parents.

Intrafamily loans let one family member lend money to another, a parent to a child, a grandparent to a grandchild, at an interest rate that is typically well below what a bank or mortgage lender would charge, while still satisfying the IRS's requirements for a bona fide loan.

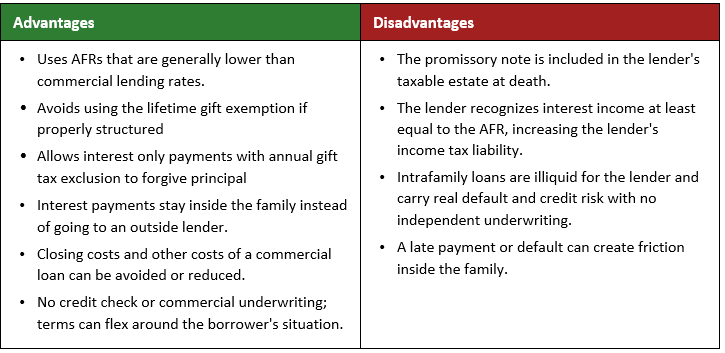

A properly structured and managed intrafamily loan has many benefits, including:

- Lower interest rates for the borrower compared to commercial lending rates

- Option to structure loan as interest only to reduce cash flow obligations to borrower

- Interest costs paid by the borrower stay within the family (possibly inherited in the future)

- No recipient credit checks or reporting

- No loan closing costs to the recipient

- Better rate of return than cash for the lender

- Ability to refinance easily if rates go down

Intrafamily loans tend to make the most sense for families who:

- Have excess liquidity and won't jeopardize their own financial security by tying up funds in a note to a family member.

- Have exhausted, or plan to preserve, their lifetime gift/estate tax exemption for other planning and would rather not use it up on an outright gift.

- Want to help a child or grandchild who can't get attractive commercial financing or want a rate below standard commercial lending rates.

To be respected by the IRS as a loan and not a disguised gift, an intrafamily loan generally needs:

1. A written promissory note that identifies both parties, the amount borrowed, the interest rate, the repayment schedule, and what happens on a late payment or default.

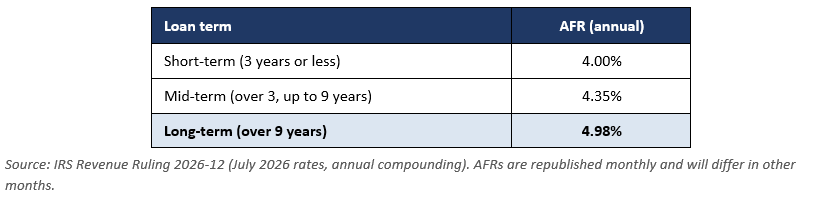

2. A market rate of interest, at least the IRS's published Applicable Federal Rate (AFR) for the loan's term, if the loan exceeds $10,000. Charging less than the AFR risks "below-market loan" treatment, which can trigger both gift and income tax consequences.

3. A genuine expectation of repayment, evidenced by actual payments, proper reporting of interest income, and documentation (dating, signatures, witnesses) that looks like any other lending contract.

The IRS publishes AFRs monthly under Internal Revenue Code Section 1274, broken into three terms based on the length of the loan. The lender chooses the AFR that matches the loan's tenure and compounding frequency.

Helping a child or grandchild buy a first home is one of the most common reasons families consider an intrafamily loan today. The starting point for many families is the annual gift tax exclusion, $19,000 per giver, per recipient in 2026 which lets a gift of that size pass with no gift tax consequences and without touching anyone's lifetime exemption. Because the exclusion applies per individual, two parents could together gift a child $38,000 or $76,000 to a child and his/her spouse in 2026 free of gift tax. That can meaningfully offset a down payment, but on its own it rarely covers the cost of a home.

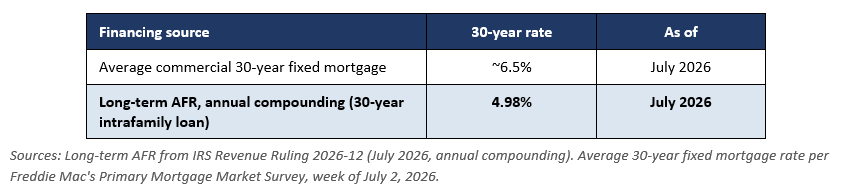

For families who want to help with more of the purchase price without triggering gift tax, financing the home through an intrafamily loan is a natural alternative. What makes this version of the strategy attractive right now is the gap between the AFR and prevailing mortgage rates.

A roughly 1.5-point spread between a long-term AFR and an average 30-year mortgage translates into real savings for the borrower over the life of a loan, and it gives the lender a return that can exceed what they'd otherwise earn on cash or short-term instruments. Interest the borrower pays on an intrafamily mortgage is generally deductible in the same way commercial mortgage interest is, as long as the loan is used to acquire a residence and is properly recorded as a lien against the property. Additionally, the lender can charge an interest only rate and use the annual gift tax exclusion of $19,000 or $38,000 for a couple to forgive the principal each year. The loan can be completely forgiven over time by utilizing the annual gift tax exclusion each year while the borrower only pays interest.

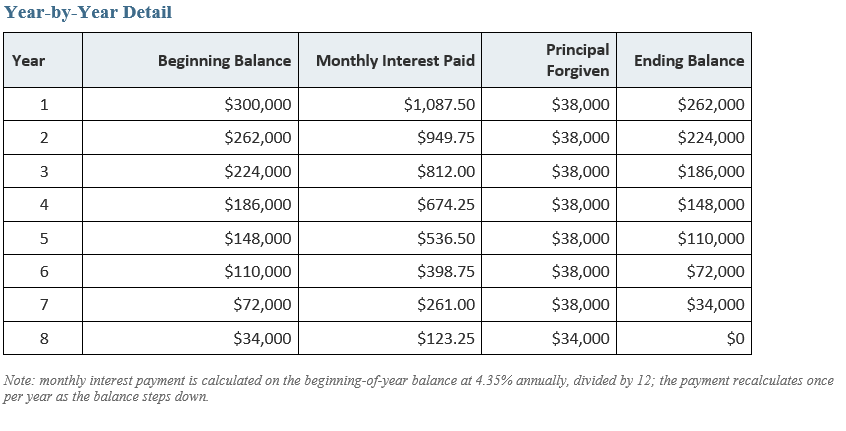

The following is an illustrative example of how an intra-family loan can combine market-rate interest payments with the annual gift tax exclusion to pay off the loan over time.

The Scenario

- Loan amount: $300,000

- Term: up to 9 years (mid-term AFR bracket)

- Interest rate: 4.35% (July 2026 mid-term AFR, annual compounding)

- Structure: interest-only, with the borrower making monthly interest payments

- Each year, the lender, a married couple, each gifting $19,000 forgives $38,000 of principal, using the full 2026 combined annual gift tax exclusion

Just as with a commercial mortgage, an existing intrafamily loan can be refinanced when rates move enough to make it worthwhile by redrafting the promissory note at a new rate and having all parties sign off. Refinancing to a lower rate reduces the borrower's cash-flow burden. Given how much mortgage and AFR rates have moved over the past several years, it is worth periodically checking whether an older intrafamily note still reflects current rates or whether refinancing it would serve the family better.

Intrafamily loans remain one of the more flexible tools available for helping family members afford a home, precisely because they don't require using any lifetime gift or estate tax exemption. The tax benefits depend entirely on the loan being treated as a genuine loan with a written note, an AFR-based interest rate, real payments, and proper reporting.