Third Quarter Market Update: Storm Clouds Forming

THIRD QUARTER EQUITY MARKETS

U.S. Markets

The third quarter saw equities go from modestly positive in July (S&P 500 rose 3.2%), to silghtly negative in August (S&P 500 fell -1.6%), to unfavorably negative in September (S&P 500 fell -4.8%). Sentiment turned wary after a strong double-digit gain in the S&P 500. We noted that that gains were largely brought about by just a few stocks, as we highlighted in our second quarter market review.

Through the first nine months of the year, the S&P 500 is still holding onto a strong 13.1% return, followed closely by midcap U.S. stocks with a 13.0% total return. Emerging markets and REITs were at the bottom of the rankings, and real estate turned negative for the year as interest rates rose.

From a sector perspective, only two sectors of the S&P 500 reported positive third quarter returns, energy and communication services. Information technology, posted a 5.6% decline after a blisteringly strong first half.

International Equities

Returns outside of the U.S. were also muted in the third quarter. The hype of China’s reopening after COVID restrictions were lifted in early 2023, has not come to pass. The Euro-region, which relies on exports to China, has seen GDP growth suffer with the lack of international demand. The latest GDP forecast for the European Union assumes growth of only +0.8% in 2023. The ECB continues to grapple with inflation, and the region is not past the peak like the U.S. In Europe, service inflation is still rising as shown below. Like the Fed, the ECB also hiked rates by 0.25% points in their September meeting.

THIRD QUARTER BOND MARKETS

The bond market saw yields rise sharply in September (and prices fall) after absorbing the Fed’s lastest statements on stubborn inflation and the probability of continued rate hikes to combat it. Since the end of the second quarter, the yield on the 10-year treasury rose almost a full percentage points from 3.8% to nearly 4.8% today.

With a rise in rates, prices fell, and the bellwhether Barclays U.S. Aggregate Bond Index fell -3.2% in the third quarter, pushing the full year return to slightly negative -1.2%.

While the yield curve is still inverted, it is less so as short-term rates have held steady and long term rates have risent this year. As you can see from the 10/9/23 blue line yield curve below, the curve has flattened out since December. The yields on the 3, 5, 7, and 10-year bonds are almost the same at 4.8% today. The inverted curve means you are getting a better rate (yield) to keep your dollars in short-term bond instruments than you are for longer-term ones, but now that trade-off is narrowing. At some point, we expect the curve to take a more normal upward sloping path where you get paid more to lock in your money for longer. We are getting closer to the point where locking in longer-term rates may be beneficial because short-term rates will fall when the Fed begins to ease.

Municipal Bond Market

Municipal bonds rates followed Treasuries rates higher in the third quarter. Tax-exempt rates rose as much as 0.57% during September alone and finished the quarter about 0.70%-0.90% higher than the second quarter. History suggests that rising municipal yields should create more investor demand in coming months, which should in-turn, create a more upwardly sloping municipal yield curve. The yield curve for municipal bonds is not inverted in the longer-dated maturities (over 7 years) and has an upwardly sloping (normal) curve.

EMPLOYMENT PICTURE

The jobs market continued to post positive monthly gains, albeit at a slower rate than 2022. However, the latest jobs report released October 6th posted a large upside surprise with 336,000 new jobs created versus expectations of 170,000. The prior months were also revised upward. This report was puzzling to many economists (and likely Fed presidents) who assumed that after a year and a half of interest rate hikes, we would see job growth materially slow. This has not been the case. The good news was wage growth was not terribly inflationary, coming in at a +0.2% increase in September month-over-month.

The job openings (JOLTS) report for August was released in early October and showed that new job openings actually rose, reversing a trend. Despite higher rates and sentiment pointing towards an impending recession, U.S. companies were adding jobs. The Fed’s softening labor market theme is just not happening. It will be interesting to listen to the Fed after the November FOMC meeting regarding the employment situation that has held up much better than many expected.

INFLATION

August Consumer Price Index (CPI) showed that inflation has slowed sharply. Both CPI and Core CPI (ex food/energy) were up 3.7% year-over-year. From the previous month, growth for CPI was +0.6% and +0.3%, respectively. The chart below from the Bureau of Labor Statistics shows the decline in 2023 from the peak CPI print of 9.1% as of June 2022. In conclusion, disinflation is working its way through the economy, but it is uneven with pockets of weakness and strength alike.

CONSUMER

We may have started to see the consumer pulling back a bit on spending. All that pent-up consumer demand post-COVID was a main reason U.S. GPD growth has been more resilient. However, Citigroup’s tracking of credit card spending shows a dramatic slowdown in September. The latest week showed a nearly 11% decline week-over-week in the 16 sectors they track. That was the fifth consecutive weekly decline in this index. Dovetailing the Citigroup data was the release of September U.S. Index of Consumer Sentiment which fell to a reading of 68.1 in September, down from 71.6 in July. The Consumer Confidence report also stalled out dropping to a 103 reading from 108 in August.

SANDY COVE ASSET ALLOCATION MOVES

During the third quarter, Sandy Cove made the decision to eliminate the small position we allocated to real estate in client portfolios. Much has changed in the 2023 interest rate environment and the Fed’s outlook to keep rates higher for longer will hurt interest rate sensitive sectors, such as real estate. In addition, office and other categories of the market face secular challenges that we need to see factored into the valuation before returning to this sectors as an investment diversifier in portfolios.

ONE MORE QUARTER IN THE YEAR 2023

We continue to be encouraged by the slowing inflation figures and a still resilient labor market. There is a constant bull/bear debate to be heard on the subject of recession: hard or soft landing of the economy. We still believe we can avoid a long and difficult recession, but we are definitely seeing a slowdown in the economy that we call storm clouds appearing on the horizon, not a hurricane. Many recession indicators like the inverted yield curve, lower housing permits, stalled wage growth, retracted money supply, and widening credit spreads are all pointing to the risk of a recession. Of note, many of these indicators have been “flashing yellow” for over a year now and GDP has been running at about 2.0%, so these indicators are either very early or wrong!

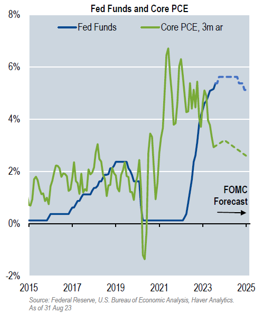

We believe the U.S. consumer will begin to tighten their purse-strings and consumption will slow in the fourth quarter, which will bring GDP below 2.0%. Additionally, the Fed’s stance of “higher for longer” has removed a lot of optimism of Fed cuts in 2024. Their latest forecast actually took two interest rate cuts off their 2024 forecast. The latest Fed thinking on rates is shown by the blue dotted line shown below.

Many, including us, were surprised at the strength of the technology rebound in the first half of 2023. This exuberance may have started to fade. Tesla, Apple, and Microsoft, to name a few of the high flying names in 2023, have been negative for the last three months. With valuations in technology still lofty and longer rates rising, we would not be surprised to see more of a pull back in the space.

Over the next two months markets will have a lot to digest including: corporate third quarter results and guidance, two monthly CPI inflation reports, another jobs reports, a potential government shutdown, a November FOMC meeting, ongoing war in Urkraine, and the unknown geopolitical risk of Middle East tensions. We could see some volatility as the markets determine the underlying health of the economy and any change in sentiment from the Federal Reserve.

As always, we will be keeping abreast of the markets so please reach out if you would like to have further discussions with our team.