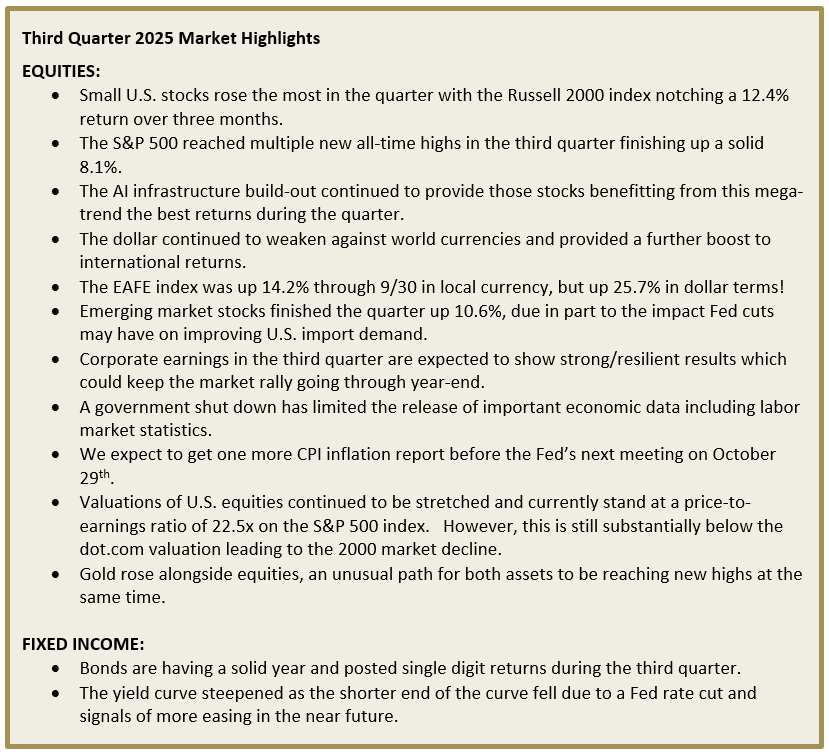

Rate Cut Added to Bull Market

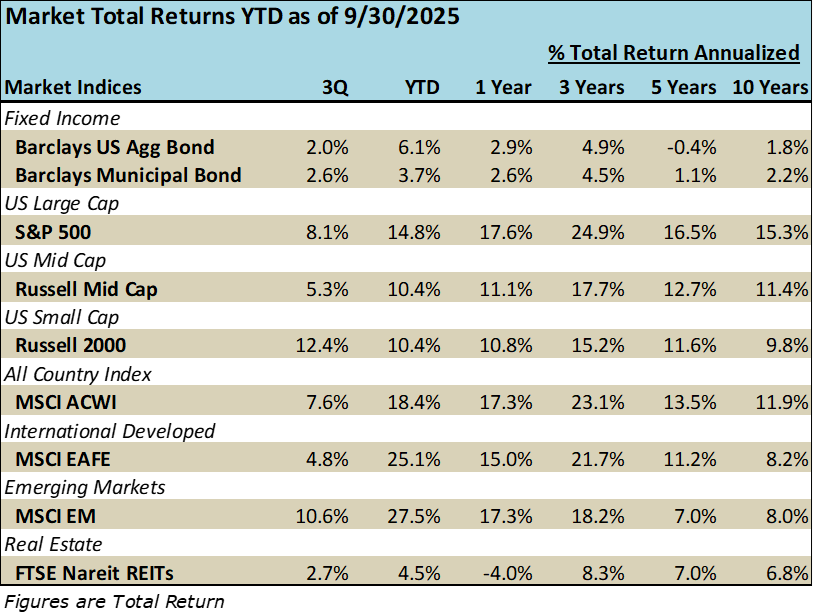

Financial markets continued their upward momentum in the third quarter as tariff worries eased, and the Federal Reserve cut interest rates and signaled more to come. The S&P 500 index is up 35% from April lows and markets show no sign of fatigue as we enter the last quarter of the year.

We continue to be in an AI infrastructure-led market, but there is market breadth outside of this important growth trend. Other economic sectors such as financial, industrials and utilities have returned double-digits year-to-date. Between the benefits of AI productivity already in use and the dovish Fed, we see a positive outlook for stocks and bonds for the next 6-12 months.

Lastly, at our latest Investment Committee Meeting in October, we made some allocation changes that we wanted to share with you which are described in detail at the end of this update.

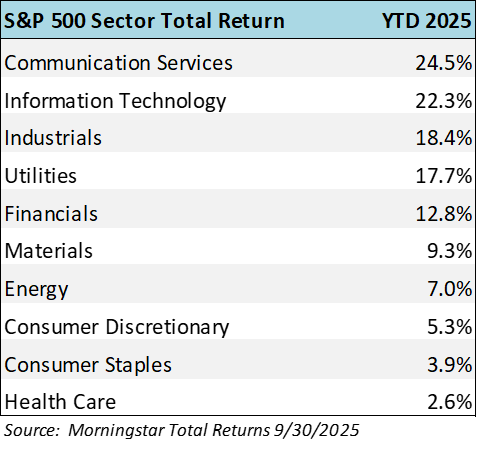

All sectors of the S&P 500 are up year-to-date, with the AI fueled ones at the top of the list below. Healthcare is the laggard due to Medicare inflation impacts on insurers and Trump’s move to curb drug price increases.

ECONOMIC DATA

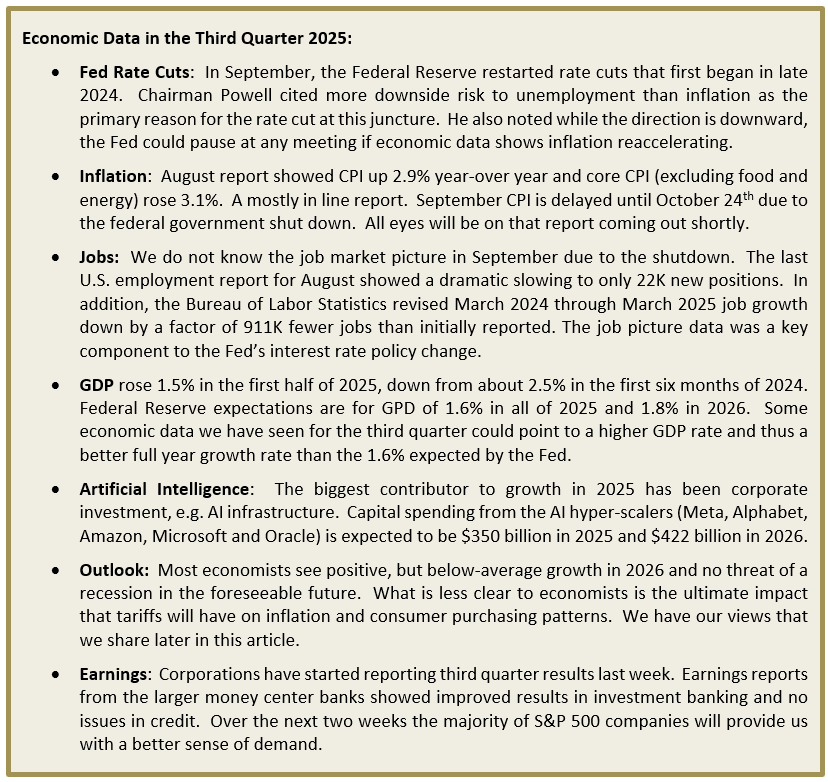

With the government closure still in effect at this writing, we are missing some key economic indicators that give us a window on how the economy is faring intra-year. There could be market volatility around these news releases when they occur (government funding dependent).

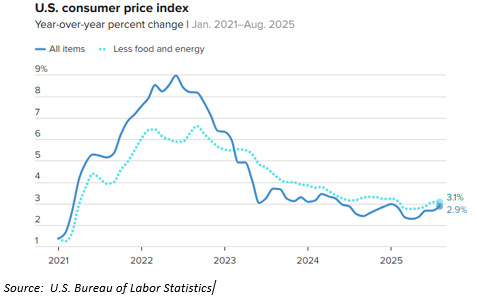

INFLATION: The latest read on inflation was in line with expectations and low enough to move the Fed off its interest rate pause. While we do believe consumers will see some price increases due to tariff inflation, it is still not showing up in the data. The last 12 months of CPI data has been steadily in the 3.0% range, as the chart below displays. Note that this data is a month old since the September CPI was not reported on time.

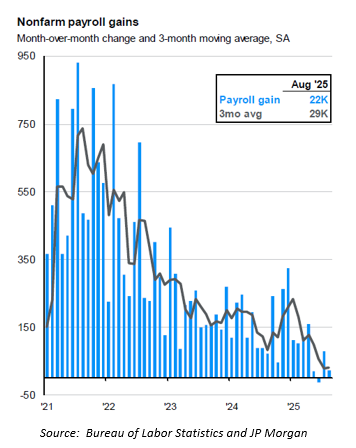

JOB GROWTH: As noted, we saw a large adjustment to the monthly figures from the Bureau of Labor Statistics which meant job creation was much weaker than we were led to believe. As you can see from the payroll table below, there has been a distinct slowdown in job growth in 2025.

SANDY COVE INVESTMENT ALLOCATION SHIFTS: We had a productive Investment Committee meeting in October where we discussed and implemented a few investment changes to further align our client portfolios to our current investment outlook.

Tariffs, the U.S. deficit, Fed policy, AI capital spending and the decline of the U.S. dollar were five main macroeconic factors that led our committee to make changes in how we allocate our clients’ investment assets going forward. We note that these changes are easy to make in retirement portfolios where we do not have to concern ourselves with capital gain tax liabilities. However, within taxable accounts, we may need to phase into these changes over time in order to limit the capital gain.

These changes are a modest shift on balance, as we are happy with our investment choices. Put simply, we have added an inflation protection investment vehicle in portfolios, increased the weighting of international equities, added to our Berkshire Hathaway position in large cap, and increased the fixed income duration exposure for clients with bond allocations. Our rationale for these changes are as follows:

NEW INFLATION PROTECTION: We are in the camp that a part of tariffs will ultimately be passed onto the end-consumer. We expect tariffs add to CPI in 2026 and beyond, we just are not sure what that magnitude will be. We also see no material decline in the federal deficit and expect conservative allocators to move towards or stay in gold versus U.S. treasuries. We decided to add a non-correlated asset that does well when inflation is even slightly elevated, like it is today at 3.0%. The fund, which we owned in 2022 when we believed inflation was not transitory, owns Treasury inflation protected securites (TIPS), gold, real estate, commodities and foreign currency. These positions are also less correlated to equities, which was also a goal in trying to add meaninful diversification to portfolios. We added a 5% position to this strategy (PIMCO Inflation Response Multi-Asset Fund) in client portfolios.

ADDED TO INTERNATIONAL EQUITY WEIGHT: We had been actively underweight international stocks for a number of years favoring U.S. exceptionalism. The overweight to U.S. equities was additive to performance for multiple years. That changed in April 2025 when import tariffs were announced and U.S. lost the performance lead over European markets. The dollar started to decline and we believe this will continue to hold for a number of years. Thus, we thought it was prudent to get back to our long-time neutral weight in non-U.S. stocks. This means adding about 5% back to international equities (in an all equity portfolio) and taking that out of U.S. large, mid and small cap stocks, pro-rata.

BERKSHIRE STOCK ALLOCATION INCREASE: Given the implicit weighting of AI within the index, we did not want to further add to our overweight position in of these stocks. We chose increase Berkshire Hathaway which has a long history of owning high quality companies. Berkshire’s ownership of insurance, utilty, and manufacturing companies help diversify our large cap allocation as well. Berkshire’s major stock positions include companies such as Apple, Bank of America, American Express, Coca-Cola, and Kraft Heinz. We increase this position size by 2% across portfolios.

We also discussed the merits of keeping our passive exposure to the S&P 500 at its current levels. We expect that AI will continue to be an important driver to U.S. growth and investments over the coming years and we are not worried of an impending bubble or overspending in this new technology (yet).

BOND DURATION SHIFT: With the Fed once again focused on monetary easing and lowering the Fed Funds rate, we expect cash vehicles like money market funds and 0-6 month bonds to also have lower yields. With the expected steepening of the yield curve, we decided to remove our one-third weighting to ultra-short term bonds entirely and focus on owning equal parts of short-term and intermediate bonds.

We have started transitioning portfolios to our new asset allocation weighting. To better understand these shift, we illustrate the weight changes in a 70/30 growth allocation portfolio as follows:

FIXED INCOME: Added 5% inflation protection and removed ultra short term

EQUITIES:

LARGE CAP: Overall falls by 2.4%, but BRK stock rises to 7.0%

MID CAP: Reduced by 0.7%

SMALL CAP: Reduced by 0.3%

INTERNATIONAL EQUITIES: Increased by 3.4%

As we enter the last quarter of 2025, we are once again pleasantly surprised at the strength of equity markets here and around the world. We see first hand the benefit that growth has had in our clients’ portfolios.

A strong investment cycle in artificial intelligence combined with interest rate easing and solid corporate earnings are factors that keep us optimistic about future market returns. We are acccepting that with growth, comes volatility. We certainly saw that in April 2025, but we stayed the course with our investment approach and that was a big benefit to clients as markets rebounded and continued to hit new all-time highs this year. We hope the fourth quarter will end on a strong note as well.

As always, please reach out to us if you have any questions.