November Market Update: Markets React Positively to Certainties

November 2020 Snapshot

|

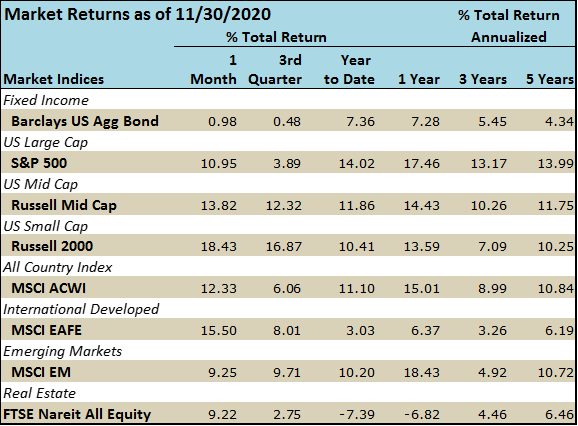

NOVEMBER EQUITY MARKETS: Equities embraced the clarity of the elections and vaccine news and rallied the entire month. November was certainly a “risk on” month with U.S. small caps returning over 18% - the best ever one-month result for the Russell 2000 index. We also saw a trade into cyclicals in the hopes of worldwide economies re-opening in 2021. Energy, financials and industrials were the top three performing sectors of the market while the defensive/safe havens of healthcare, consumer staples and utilities were the three lagging sectors in November.

Outside the U.S. the developed countries outperformed both the U.S. and emerging markets with a strong 12% return for the index. Spain, Austria, Poland and Greece all turned in monthly returns over 25%!

As we’ve mentioned in previous market writings, we still believe international markets will provide long-term opportunities for investment growth given the valuation and growth gap between the U.S. and international stocks. On the valuation side, the S&P 500 has a forward price-to-earnings ratio of 21.8x versus the non-U.S. stocks (ACWI ex-Us) of 16.5x. This implies that the market is valuing non-U.S. stocks 24% cheaper than U.S. stocks. A 20-year history of price-to-earnings is much narrower with the U.S. average P/E at 15.4x versus the ACWI-ex U.S. at 13.5x.

Additionally, earnings growth for the MSCI EAFE Index is projected to be higher next year than for the S&P 500. We believe earnings growth is typically a leading indicator of outperformance in equity markets and continue to believe an allocation to international stocks will benefit long-term performance.

BOND MARKETS: The yield curve flattened slightly during November as the longer dated bonds fell while the short-term rates held steady. The 10 Year Treasury yield dropped 2 basis points to 0.84% and the 30 year fell 7 basis points from October to 1.57%. Given the positive news on the elections, vaccines, Yellen’s potential appointment, all bond segments recorded positive returns for November.

Source: Baird Investment

MUNICIPAL BONDS: Muni rates fell pretty sharply in November (blue line on graph below) and prices rose. Most of this was due to the smaller supply of muni offerings during November. With demand still strong for muni supply, the imbalance pushed up prices. Looking to 2021 in the muni market, optimistic investors want to see a better revenue profile as the economy gets back to normal after we’re vaccinated. The technical aspects of supply and demand are still strong with the pull forward of new muni supply offerings before the election and the seasonally-heavy demand from the large reinvestment flows of December and January.

Source: Baird Investment

ECONOMY: Non-farm payrolls increased by 638,000 in October and the unemployment rate fell to 6.9%. As of October, the economy has regained 54% of the 22 million jobs lost between February and April. Clearly, there is still a long way to go before we get back to the full-employment we enjoyed pre-pandemic and most economists are looking out to the second-half 2021 before we get there.

Other economic indicators in October were again positive such as retail sales, consumer spending, real estate transactions, and durable good orders. Much of the positive momentum seemed to continue in November though the rising COVID-19 case count could stop that momentum in its tracks.

Inflation is still well at bay with the core rate at 1.2% and well short of the Federal Reserve’s target of 2.0%.

Odds have just increased for more stimulus. In early December, we began to see some movement on the stimulus package stalled for months in Washington. While nothing is signed into law as of this writing, Democrats appear to be coming to the bargaining table on a smaller stimulus bill. Previously, House Speaker Pelosi rejected any bill less than $2.2 trillion. Hopefully, lawmakers can provide some financial help to Americans before year-end.

COVID-19: Despite great news on the vaccine front, we are facing a second infection wave and record daily cases in the U.S. and worldwide. Talk of surge capacity at hospitals is once again on the front page of the news.

As of December 1, 2020, the 7-day average U.S. daily COVID-19 cases were over 170,000, materially higher than the initial surge of about 35,000. The chart below shows the 7-day average case count in the U.S. in addition to deaths; both of these figures are increasing in November and early December.

Source: Natixis PRCG, WHO, Johns Hopkins, Bloomberg, COVID Tracking Project Data as of 12/3/2020

It was hopeful to hear that the Head of Operation Warp Speed, Moncef Slaoui, said there should be enough vaccine supply to inoculate the entire country by June 2021. We’ll get FDA news around December 10th for Pfizer’s vaccine and then a week later for Moderna. Vaccines are already being shipped in anticipation of a positive FDA review and could be made available to healthcare workers by year-end.

We are all likely in the same boat feeling happy to be in the last month of 2020 and to put this challenging year behind us. The markets are certainly focused on a 2021-post pandemic world with the recent positive returns, the rise of cyclical stocks, and healthy credit markets. However, we must point out that 2021 may not be as smooth sailing as the markets are signaling. With the S&P 500 well above it’s 200 day moving average, we are pricing in perfection at a time of still many unknowns. Additionally, the markets crave a low-interest rate environment, like the one we’re in, but that may come to a halt sooner rather than later if inflation picks up and causes the Fed to change course and tighten. This tug of war leads us to believe we will continue to see market volatility in the short-term and will take advantage of lower equity entry points.

We wish you all a safe and healthy holiday season. As always, please reach out to any Sandy Cove Advisor colleague with questions or concerns.