From the Desk of the CIO: 3Q Market Review

Market Review 2017 3Q: In this quarterly newsletter, we are taking the opportunity to not only review the markets but to also introduce our Investment Committee and explain how they are integral to our investment process.

That was a great quarter for risk assets! Stocks just capped an eighth straight quarter of gains, the longest winning streak since the start of 2015. International equity markets again outpaced U.S. markets with emerging markets (EM) leading the way, up 8% for the quarter. The EM asset class is leading all others and is up 27% year to date (YTD). The MSCI EAFE Developed Markets Index, which is made up of mostly foreign blue chip companies (think Nestle, Novartis, Toyota, etc.), also had a strong showing – posting a 5.5% return for the quarter and a 20% YTD gain. Foreign equity markets are enjoying improving economic data and earnings expectations. A weaker US Dollar also served to make foreign goods more competitive on the world scene, which has led to better sales for these firms.

In the US, weak inflation figures caused investors to doubt the Fed’s desire to hike interest rates, leading to a 0.8% return for Bonds (US Barclays Aggregate Bond Index) for the quarter and a very respectable 3.16% YTD return. In US Equities, small cap stocks led large caps as the Russell 2000 returned 5.7% vs a 4.5% quarterly return for the S&P 500 Index. US stocks benefited from the lower for longer interest rate environment, improving earnings and hopes of a corporate tax cut. The third quarter’s benign interest rate environment also helped REITs to a 1.1% gain. Commodities had a broad resurgence after a weak 2Q and were up 2.5% for the quarter but they remain down 4.5% so far YTD.

We are cautiously optimistic here in the fourth quarter of 2017 because history has been kind when a year’s prior three quarters have been positive. Theories abound as to why the fourth quarter is often the best one for equity bulls. Fund managers need to catch up, holiday spending kicks in, investors celebrate the “January Effect” of rising stock prices a bit early. For whatever reason, the S&P 500 Index has been up in seven of the last eight years between October and December. This recent strong “seasonality” has been a force to be reckoned with. Since 2009, the S&P 500 has averaged a 6.2% fourth quarter return! Current valuations keep us cautious while we are mindful of this historical pattern of momentum.

Helping us to make sense of all of these markets is the Sandy Cove Advisors Investment Committee (IC) which is made up of the investment professionals here at Sandy Cove and three other professionals with very strong investment backgrounds (Kate Saltonstall, Dan Butler and Maureen Depp). Our last meeting was held on October 4th at our offices in Boston. At this meeting, the committee came to a number of important conclusions regarding “Active” management, the direction of interest rates and rightsizing our international equity weighting.

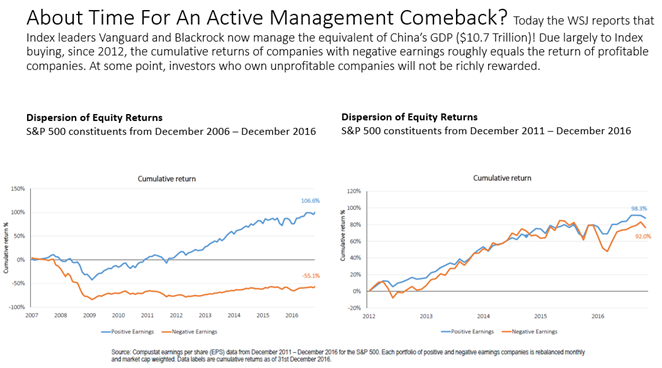

On the question of “Active” vs “Passive” management, we have answered “both” in the past. Depending on the asset class, our skew of active and passive investments varies. However, due to the extreme amounts of cash chasing index investments, as fiduciaries, we feel our clients will be best served with a healthier skew to “active” going forward. As the chart below (from our IC meeting) highlights, the blind buying of index funds since 2012 has led to a situation where unprofitable companies have virtually the same return as profitable companies. Good active managers should be able to differentiate themselves in this environment going forward.

On the direction of interest rates, our Investment committee had a strong consensus of thought that interest rates would rise only modestly in 2018. We project the US 10 year Treasury bond yield to rise from 2.30% to 2.75%-2.90%. Given this moderate rate rise, we feel it is best to leave the management of duration to our active bond managers. Since our Manager Selection Screening process has done a very good job in selecting outperforming managers, we believe it is best to give these managers a relatively free hand. However, we believe that our bond average maturities should be a year or two short of the 7-8 year index average to protect capital if rates rise more than we expect.

On the question of our International equity weighting, the IC decided to raise our exposure across all of our asset allocation models. We initiated this discussion with an acknowledgement of the fact that roughly 50% of the world’s equity market capitalization is non-US. We also highlighted the fact that for significant periods of time, over the past few hundred years, International stocks have outperformed US stocks. In the relative short term, since 2012, International stocks have lagged their US counterparts by a wide margin (see chart below). Today, the valuations of International equities are well below their US counterparts by several measures. For example, according to FactSet, International Developed stocks (MSCI EAFE Index) trade at nearly half the price of the S&P 500 as measured by the current Price/Book Value ratio. Those same International stocks pay a 3.03% average dividend while the S&P dividend is 1.95%. Our manager selection process identified two great international active managers that have provided us with robust returns. We’ll be adding to these managers in coming days.

We’d be happy to pass along the full recap presentation from our last investment committee meeting to all those who wish to have a copy. We are ready to discuss any individual, more pointed questions, you may have as well. Best wishes for a great 4th quarter and holiday season.