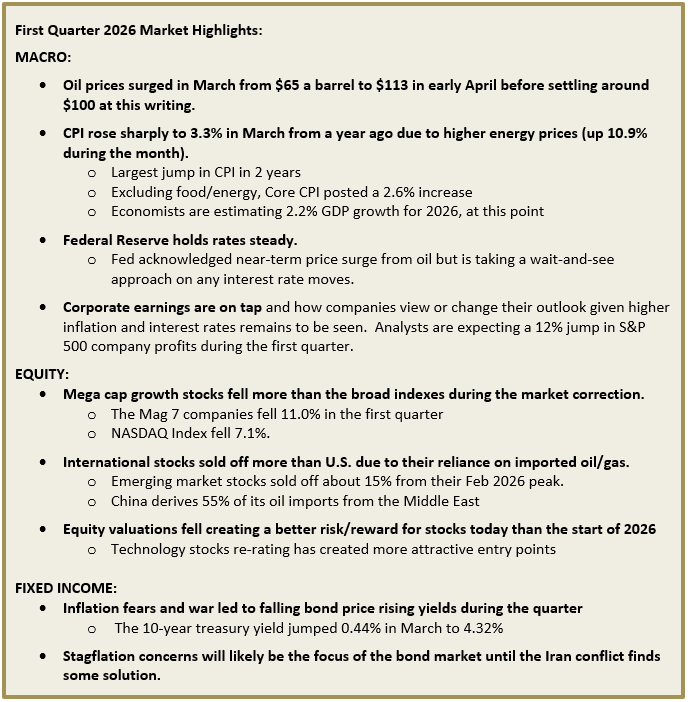

First Quarter 2026: Markets React to Iran Conflict

The first quarter was mostly defined by the month-long invasion of Iran by the U.S. after failed diplomatic talks. Volatility reigned supreme. Oil prices rose sharply as Iran closed the Strait of Hormuz to tanker traffic thereby creating a supply chokehold. Equities around the globe sold off in March with most indexes falling into correction territory (down by 10% or more from recent peaks). The last day of the quarter saw a sharp stock and bond rally in hopes of war de-escalation. We believe we are still in a period of heightened volatility.

Prior to the geopolitical fighting, there was a lot of good news on the horizon for U.S. economy and equities. Corporations were expected to report double-digit earnings growth for the first quarter, we expected to see the AI productivity enhancements across many sectors, and stimulus, by way of income tax refunds, was about to benefit the economy as well. Then the bombing of Iran started on February 28th and focus turned to what is not working versus what is. Still, we believe the markets have been remarkably resilient thus far. As we have noted before and in our “FLASH REPORT” on March 30, 2026, clients are mostly rewarded for staying the course and not selling during geopolitical events.

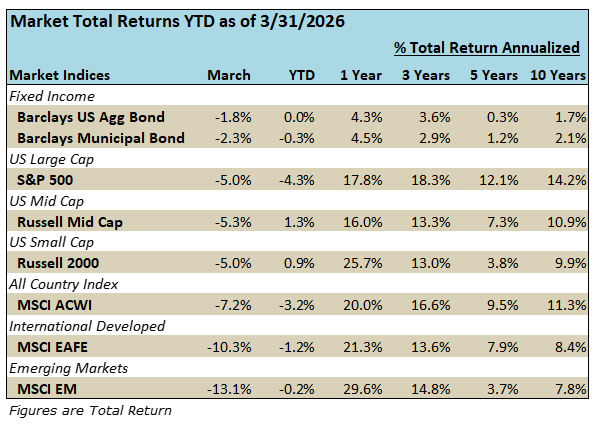

As the table above illustrates, March was a down month with not many places to hide. Even “safe haven” gold fell 11% during the month. U.S. indexes performed better than international counterparts due to our net energy exporting status. The bell-weather S&P 500 index fell 5% in March and posted a modest 4.3% decline for the year-to-date ending 3/31/26.

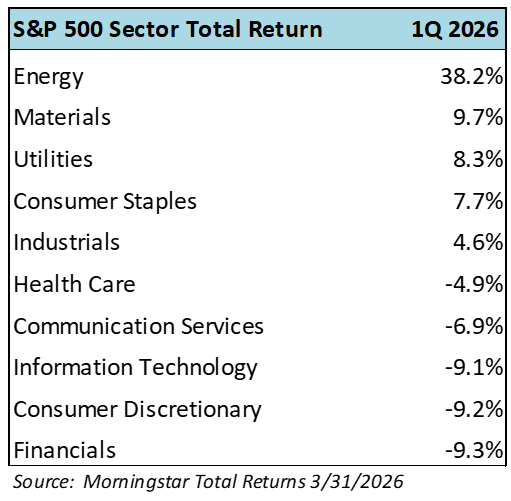

By sector, the clear winner was energy with those stocks in the S&P up 38.2% in the quarter. Sector laggards included large cap technology holdings and financials (see Sector Return table below).

We’ve been here before with this administration’s policy surprises. Last year about this time was the tariff announcements, this year a 6+ week old invasion of Iran. Both decisions weakened markets in the near-term. While this time feels worse, the decline in equity markets thus far is much lower than the first month of the tariff-induced correction in April 2025.

As we know, Trump negotiated with trade partners well below the initial tariff amount only to have the executive order ruled unlawful by the Supreme Court less than a year later. Markets not only recovered from the April/May 2025 lows, but went on to have a solid year. We did not make any near-term reactions to asset allocation during either of these episodes. Last year, that proved to be a good course of action given the markets’ rebound.

This year, we are still holding course on overall asset allocation, but we have made two changes to our portfolios for other reasons.

1) We further added to our inflation response strategy this spring. This was fortuitous given the rise in oil prices, but we already had a 5% weight in most portfolios last fall. We have since added a few percent more to this strategy as we believe that the 2.0% inflation rate goal will not be achieved this year.

2) We also lowered exposure to a mid-cap active manager. Performance over a 10 years period was stellar for this 5-star Morningstar ranked fund. Through March 2025 it ranked in the 5% percentile of all mid cap growth funds with a annualized return of 12.1% from 2015 to 2025. However, it had a difficult year in 2025 and we determined the best course of action was to cut the position in half, where appropriate for clients. We used the proceeds to purchase a low-cost mid cap index fund.

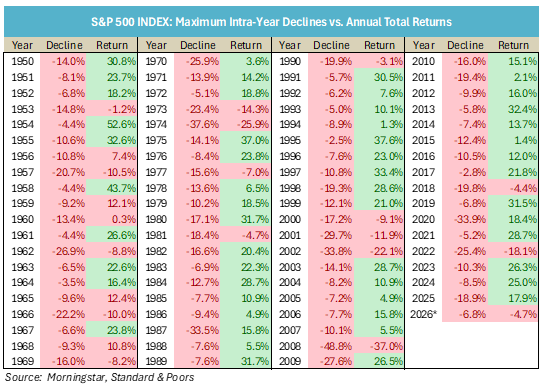

While the daily events surrounding Iran and the Hormuz Strait take up most of the headlines, we are patiently using market dips to put excess cash to work for our clients. Market corrections are a natural part of investing (you have to take on some risk if you want the return) and we just saw a modest drawdown in March. The chart below demonstrates that every year the S&P index sees some intra-year decline and it rebounds the majority of the time.

As we enter the early days of spring in New England we are invigorated by the renewal we see all around. Like the markets, it is not all systems go right away in our neck of the woods, but we do see some green shoots that we are cautiously optimistic about.

As always, please reach out to us if you have any questions.