August Market Update: Powell is Not Convinced

AUGUST EQUITY MARKETS

Equity markets started the month on a positive note, but fell into negative territory in response to Chairman Powell’s comments surrounding rate hikes. Markets reassessed asset prices as if central banks will continue to raise rates higher to combat stubbornly high inflation (increasing the denominator of the pricing equation). Investment firms are not crying recession yet, thanks to recent upbeat data, but the market has certainly pulled back in the final days of the month. There is a large amount of geopolitical risk keeping volatility high: Russia-Ukraine war continues, impacting energy and food supply; Europe shows recessionary signs as it experiences an energy crisis due to unreliable supply from Russia; and China reacts to an uptick in cases by restarting lockdowns in some regions, slowing output. Exogenous forces continue to paint an uncertain future for energy, input prices, and upstream supply chain speedbumps from China.

The more growth-oriented health and tech sectors were most impacted by the concerns surrounding rate hikes. Meanwhile the energy sector continues to have an excellent year of returns.

FED POLICY: FEARS OF INFLATION BATTLE WITH FEARS OF RECESSION

For yet another month, we cling to each word that Fed Chairman Powell speaks. At the Jackson Hole Summit towards the end of the month Powell said, “we are moving our policy stance purposefully to a level that will be sufficiently restrictive to return inflation to 2%.” The decelerating inflation numbers from July were not compelling enough to reverse the hawkish tone. He also said that the economy might “feel some pain” and that the “Fed will use it tools forcefully.” In response, the market factored in another 0.75% hike at the next meeting, September 21st, and continues to weigh the reality that Powell prefers a hard economic landing to runaway inflation.

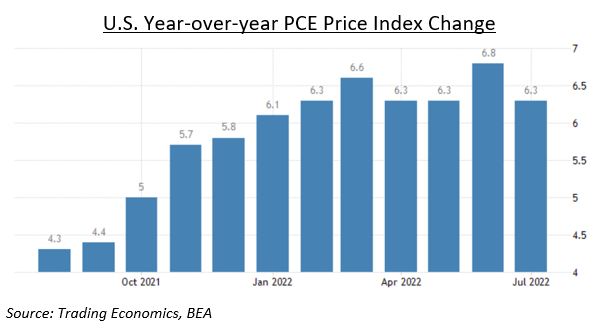

Ultimately, the Fed will be data dependent on the speed and magnitude of their tightening. While headline PCE was encouraging, the core PCE moved up slightly, displaying the stickiness of shelter and wage inflation. In the first days of September, the August jobs report came in right around expectations which means that we dodged a surprise to the upside or downside and the market expectations hold. We will keep an eye on the spending patterns to start the fall season when people come back from summer vacation and pay attention to their finances more closely.

We have been saying this since the start of the year and it still rings true: expect volatility through the changing economic conditions and midterm elections. Even with short term pains and fluctuation, the common enemy is still inflation and the Fed is still our most powerful tool.