2023 Market Outlook: Prospects Brighten as Fed Slows

Last year, we titled our outlook piece “Year of Fed Tightening” and put the focus on the Federal Reserve because we believed it held the majority of control over the path of the economy and the markets. We were spot on with that assessment as more attention had been on the Fed’s path, stance, pivots, statements, opinions, than any other economic indicator last year. We have all been on “Fed watch” to understand the psyche of all Fed governors and how they would play catch-up in raising rates to combat high inflation.

The Federal Reserve

Now we are all wondering, when will it be over? A perfectly good question to ask as we enter 2023 with multiple monthly data points showing inflation decelerating, and other economic factors pointing to a slowdown, which is the ultimate goal of the Fed. This year, markets will continue to focus on the Fed and inflation with the added concern of a recession.

The Federal Reserve continues to be “data dependent” and telegraphed that there is still more work to do. After the Fed moved the fed funds rate from nearly zero to 4.50% in quick succession in 2022, it also raised its target in 2023 for the rate to be in the 5.00-5.25% range. As of this writing, the market isn’t believing the Fed as the fed funds futures are only at 4.89% for May 2023 and the 2-year treasury, which follows fed funds closely is at 4.25%.

The market reacts quickly to economic data and has seen CPI fall for four consecutive months, contraction of both the manufacturing and service indexes in late 2022 and slowing wage growth released in early January. We believe investors will be rewarded, by paying attention to the markets versus waiting for the “all clear” sign from the Fed, because the market will probably be well off the bottom by the time information is that clear. Stocks have historically been a leading indicator of the economy and tend to rise six-nine months before an economic recovery takes hold.

Economic Picture

The Fed is doing its best, through interest rate hikes, to derail inflation and that has a side effect of throttling back the economy in the process. To what extent the Fed will be able to lower inflation and keep a recession at bay is honestly anyone’s guess. As Chairman Powell said last month, “I don’t think anyone knows whether we’re going to have a recession or not…it’s just not knowable.” However, there are numerous strategy and economic pundits with opinions from a deep recession, a soft landing, or no recession at all for 2023. The various opinions are enough to make your head spin. We won’t know who had the clearest crystal ball until sometime next year when we get the data on full year 2023 GDP. But we do know that the U.S. equity markets have already taken into consideration a lower growth (recessionary) outlook by way of discounting the markets in 2022 for an impending economic downturn brought on by interest rate hikes.

GDP Outlook

Growth will be slow, no doubt, given the Fed’s goal to do just that. Sandy Cove views Goldman Sachs Investment Strategy Group’s global GDP outlook to be close to our thinking, knowing that we are all taking educated guesses. Their views are seen in the table below and point to low growth in the US and Japan, negative growth in Europe and slowing growth in China.

Source: Investment Strategy Group (ISG), Goldman Sachs Investment Research (GIR), Bloomberg

Source: Investment Strategy Group (ISG), Goldman Sachs Investment Research (GIR), Bloomberg

On the other side of the spectrum is the more conservative World Bank, which semi-annually prognosticates on their global growth views. They are more pessimistic looking for world-wide growth to slow to 1.7% in 2023, a stark change from their 3.0% growth view in June 2022. They see the U.S. economy growing at just 0.5% in 2023 before rebounding to 1.6% in 2024. They factor in global inflation, higher interest rates, and disruptions caused by Russia’s invasion of Ukraine and key inputs to their forecast.1

We see enough strength in the job market and health of the consumer to be in the camp of a soft-landing for 2023. That means a mild recession with a few quarters of slightly negative GDP. As a reminder, we actually had two consecutive quarters of negative GDP growth (the text book definition of a recession) in 1Q and 2Q of 2022. Economists at large noted that there were some major inventory adjustments that accounted for the anomaly and no one characterized 2022 as a true recession year.

Job Market

The U.S. economy had the second-best year of job creation since 1940 adding 4,500,000 people to the payrolls and bringing the unemployment rate down to a historically low of 3.5% as of December 2022, according to the Bureau of Labor Statistics.

Its resiliency is both a blessing and a curse. It is a blessing because a fully employed workforce is earning wages and consuming goods, which is a key factor in the camp seeing little to no recession in 2023. It is a curse, because a tight labor market usually means wage rates may need to rise to entice workers into jobs. The Fed’s biggest fear in 2023 is a wage/price upward spiral. The Fed needs to see slack in the labor force before it pivots from its tightening stance. This is hard to imagine given the supply of labor versus the tremendous number of job openings. The latest JOLTS report (Job Openings and Labor Turnover) from the Bureau of Labor Statistics showed that in November there were 10.5 million job openings, or 1.7 available positions for every person seeking work.2 The Fed would like to see the ratio much more in balance and the monthly JOLTS data will be an important figure for the Fed to watch.

On the bright side, we did see some good news in the latest jobs report that showed a deceleration of wage growth in the December data. Average hourly earnings for all employees on private nonfarm payrolls rose by + 0.3%, versus a hike of +0.6% in November. If wage growth moderates or even declines from last year’s levels over several months, it will give the Fed partially what it is looking for to stop hiking rates.

U.S. Consumer

Excess savings created from lower demand during the pandemic and stimulus checks have mostly worked through the system as the chart below illustrates.

Source: JP Morgan, Guide to the Markets, 1Q23

Source: JP Morgan, Guide to the Markets, 1Q23

We witnessed a rebound in demand for goods, then services and found ourselves paying more for everything as well (hello, inflation). Still, the U.S. consumer has prevailed and is in a healthy position regarding household net worth and household income. U.S. consumers are in an enviable position versus many international counterparts because they are mostly employed and earning higher wages than a year ago. And despite high inflation, it is not as bad as Europe where more disposable income is being spent on much higher energy inputs.

The chart below shows just how important the U.S. consumer is to the health of our economy. It drives over two-thirds of GDP.

Source: JP Morgan, Guide to the Markets, 1Q23

Source: JP Morgan, Guide to the Markets, 1Q23

There has been clear evidence of an economic slowdown in the back half of 2022 and we expect that to continue into 2023 as the larger interest rates hikes begin to work their way into the economy. Below are some other important economic statistics that we watch that are flashing yellow or are already in contraction territory.

Other Key Economic Stats in the U.S.

- Conference Board’s leading economic indicators fell in December for second month in a row

- Housing permits, new home sales and mortgage applications all fell sharply as mortgage rates rose

- U.S. Manufacturing Index has contracted two months in a row and stands at 48.4% in December

- U.S. Services Index contracted in December, the first time since the pandemic with a reading of 49.6%

- Consumer Sentiment Index hit a low in December not seen since the great financial crisis in 2008

- Monetary supply has tightened with Fed hikes and reduced bond buying

- Yield curve inverted in 2022 and is still inverted today

Source: Wall Street Journal January 7, 2023

Source: Wall Street Journal January 7, 2023

Corporate Earnings Growth

Currently Wall Street expects earnings for the S&P 500 to be around $226 per share. We think this is slightly too high and will likely see it reduced in the January/February time frame when most public companies report their December quarter results and provide profit guidance for the upcoming year. We expect S&P 500 earnings to grow in the mid-single digits this year to about $215 per share. We see many more sectors participating in growth and positive returns, a stark difference from last year, which we discussed in our other piece this month, 2022 Market in Review.

EQUITIES

U.S Equities

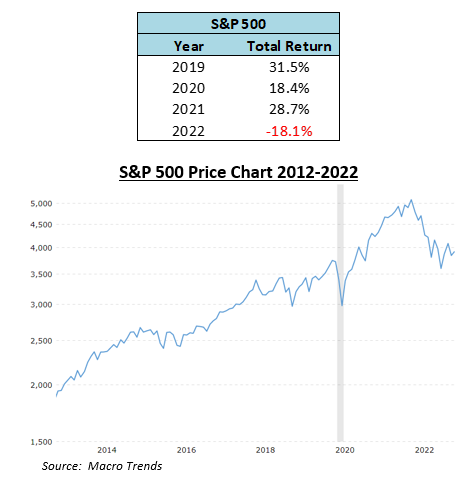

There have only been four times in history where U.S. equities have had back-to-back negative year returns, and we don’t think 2023 will bring a fifth time.3 We are in a much better position entering 2023 than we were in 2022. We have had price adjustments in the market to discount a slower growing economy. The current forward price-to-earnings ratio on the S&P 500 is 16.6x versus the 25-year average of 16.8x. We have seen aggressive Fed rate hikes that are likely in the last inning, and we think companies will recalibrate their 2023 earnings growth expectations with conservatism. These are all potential catalysts for a rebound in equities after such a difficult year in 2022 as seen by the four-year return table of the S&P 500 below. We believe the macro environment will become more supportive of equity markets and see single-digit gains or better for U.S. equities.

International Equities

International markets could have a good performance year in 2023, but that is dependent on three major things which is out of their control and nearly impossible to predict: war in Ukraine, weather, and the U.S. dollar relative to Eurozone currencies. A quick resolution in Ukraine not happening and thus is a major detractor to the regions that rely on Russia for energy. In the last few months, international equities have rebounded as the U.S. dollar peaked in September, but we don’t know if that will be a theme that will continue to play out in 2023. Additionally, a milder winter has been a huge relief to Europe, thus far, but weather is difficult to predict and cannot be an investment thesis in and of itself. We reduced our weighting in this region a few times in 2022 and if we believe dynamics, fundamentals, and valuations have improved, we would look to add back to this region in 2023. This will be a key discussion at our upcoming Investment Committee meeting in the first quarter.

Energy Shock Hurts Income Outlook in Europe

Source: Goldman Sachs Economic Research, November 2022

BONDS:

We are finally looking at a year where we will get some real income from our fixed income investments. Higher yields (thank you Federal Reserve) have made a comeback and high-quality fundamentals in the corporate and municipal credit spaces will likely make 2023 a good year in fixed income after the worst year the Barclays Aggregate Index has ever had. The table below illustrates the point that fixed income is starting the year in a much better place, from a yield perspective. This is important because yields have been a leading indicator of returns.

Municipals bonds are still attractive versus corporate bonds or treasuries for those in tax brackets of 32% and higher because the after-tax yields are higher. We are seeing tax equivalent yields of 8.5% in municipals for MA residents in the highest federal tax bracket. Strong yields along with good fundamentals have made us very positive on this asset class for the foreseeable future.

We have always viewed fixed income as the ballast in a portfolio. It provides diversification from equities and protection from equity market shocks and economic slumps. As of this writing, Sandy Cove Advisors continues to keep a shorter duration than the Bloomberg Aggregate Bond Index duration, which was a benefit to clients throughout 2022. We will look for opportunities to extend duration out to a more normalized intermediate time frame (4-7 years). We would look to add duration and improve yields when we believe the Fed is done tightening.

Forecast Caveats:

What could prove our forecasts wrong for 2023? There are certainly factors that could affect and/or change our market assumptions. We list our top four reasons for better or worse conditions than we’ve laid out in this piece.

In conclusion, we are doing our best to help clients navigate the uncertainty that the markets have brought to us. There are plenty of unknown risks in the world, and the best protection is to diversify and plan ahead. We continue to pay attention to our clients’ diversification through asset allocation and investment strategy selection. We expect a volatile first half of 2023 in equities where we may retest lows, but we see the market setting up for an improved second half of the year and expect slightly positive returns on the horizon. For fixed income, we expect low single-digit positive returns driven mostly from income.

As always, your Sandy Cove team is available to answer any questions about the markets or your portfolio. We wish you all a happy and health new year.