2020 Year-End Tax Planning

DOWNLOAD 2020 Y/E TAX PLANNING PDF

With the year-end fast approaching, it is time to consider some strategic moves to reduce your 2020 tax bill. This year’s market activity makes it all the more important for clients and advisors to consider tax saving strategies. Where appropriate, realizing gains, harvesting losses and considering gifts to family and charity are all tax efficient strategies.

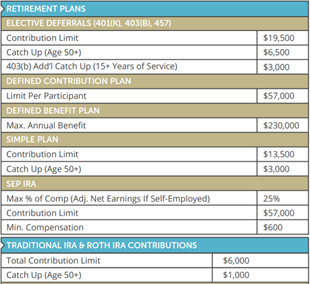

Retirement Plans

You may be able to contribute more to a workplace retirement plan this year because the IRS has increased certain limits for inflation. Take full advantage of your employee retirement plan, at least to the point of any employer match. As with your pre-tax salary deferrals, any employer contributions to your plan account are not taxed to you until distributed.

Some retirement plans allow participants to make after-tax contributions in addition to regular pre-tax or Roth salary deferrals. If you are a high earner and your plan allows it, consider making after-tax contributions with the intention of converting those amounts to a Roth IRA when you leave the plan. In workplace retirement plans and IRAs, additional contributions are available for account owners 50 years or older.

The IRS now requires most people to start taking money out of their tax-deferred retirement accounts once they reach age 72, rather than age 70, but that is on pause this year due to the CARES Act. However, if you still want to take your Required Minimum Distribution (RMD) before year-end, multiple accounts can be aggregated and the distribution can be taken from one account. The so-called RMD vacation in 2020 may push some retirees into a lower tax bracket, and that creates an opportunity for them to look into converting some of their tax-deferred savings to a Roth IRA at a lower rate than usual.

Establish and Fund IRAs for Next Generation

Help your child or grandchild get an early start on saving for retirement. Consider making a gift of up to $6,000 to either a traditional or Roth IRA for those who are not funding their own accounts, but have enough earned income to do so. Contributions to IRA’s for your family members are taxable gifts and should be coordinated with other gifts that you make during the year.

Prepay Deductible Expenditures

Standard deduction is now $12,400 for individuals, $18,650 for heads of household and $24,800 for married couples filing jointly. In order to benefit from itemizing, deductions must exceed the appropriate standard deduction amount. If it appears that the Democratic proposal to limit itemized deductions is enacted in 2021, then you may wish to more aggressively accelerate deductions in 2020, even if you believe your marginal tax rate will be higher in 2021.

If you itemize deductions, accelerating some deductible expenditures into this year to produce higher 2020 write-offs may make sense if you expect to be in the same or lower tax bracket next year.

- Mortgage Payment(s) – Accelerating your mortgage payment that is due in January will give you 13 months’ worth of deductible interest in 2020. Remember that home equity interest is only deductible if the loan proceeds were used for residential acquisition or capital improvements, and are subject to the overall home loan debt limit of $750,000 for residential debt incurred after December 15, 2017 and $1 million for pre-existing debt.

- Bunching Deductions – Consider “bunching” several years of charitable contributions into one year with a Donor Advised Fund.

- Miscellaneous Deductions – miscellaneous deductions exceeding 2% of AGI are eliminated for Tax Years 2018-2026.

Be careful if you will owe the alternative minimum tax (AMT) this year as prepayment strategies can backfire. Under the AMT rules, write offs for state and local taxes and miscellaneous deductions are disallowed. Speak with your tax advisor to see if you fall under AMT before you accelerate these deductions.

Charitable Donations

Charitable deductions are very valuable in this income tax rate environment. Consider starting a Donor Advised Fund (DAF) or contributing appreciated stock instead of cash to a charity or DAF. DAF’s allow you to front load charitable contributions into one calendar year, but pay out the money over time.

Gifting certain appreciated assets to select charities can also provide more “bang for the buck,” as you not only may get an income tax deduction based on the fair market value of the donated asset, but you would also not have to pay capital gains tax on that asset’s unrealized appreciation. Clients’ should realize the full benefit of a tax deduction in the current calendar year, which could be helpful if there has been a spike in income.

Tax Loss Harvesting

Tax loss harvesting involves selling an investment that has lost value to realize a capital loss and using that loss to offset either any realized capital gains or up to $3,000 a year in ordinary income. However, you do not want to undermine your long-term investment goals and sell investments just for tax purposes. Don’t let the tax tail wag the investment dog.

If this strategy is appropriate for you, it is important to maintain your strategic asset allocation so that you continue to participate in the market. The IRS will not allow you to write-off the loss if you purchase substantially the same investment 30 days before or after the sale. This is called the “wash sale” rule.

Capital Gain Distributions

If you own any investments in taxable accounts that are subject to end-of-year capital gain distributions, consult with your advisor on strategies to minimize the tax liability.

Estate Planning

For 2020, the Federal Gift and Estate Tax exemption is $11.58 million per individual. This exemption can be used during your lifetime to make gifts, or at death to reduce or eliminate estate taxes. However, you may want to consider using a portion of this exemption now, removing the value and any appreciation from your estate in the coming years, as these higher thresholds are likely to be reduced with our new administration.

Intrafamily Loans

With current interest rates at near historic lows, and demand with traditional lenders at all-time highs, loans among family members, "intrafamily loans," continue to be a popular means of assisting family members and keeping wealth within the family. In addition, allowing family members to avoid the constraints of traditional loan underwriting. The 2020 Blended Annual Rate is .89%, compared to 2.42% in 2019.

Annual Gift Exclusion

You can make annual exclusion gifts of up to $15,000 a year or $30,000 per couple to an unlimited number of individuals free from gift tax or without using any of your federal exemption. If you are making these gifts to an irrevocable trust, such as a life insurance trust that provides the beneficiaries with a limited withdrawal right, make sure the trustee notifies the beneficiaries and keeps the appropriate documentation (often referred to as “Crummey” Letters). Taking advantage of the annual gift tax exclusion can reduce your estate that may be subject to inheritance taxes.

Fund 529 Plans

Consider funding 529 plans by December 31 to apply 2020 annual gift tax exclusion ($15,000) treatment to the contributions. You can “front-load” 529 plans by making 5 years’ worth of annual exclusion gifts to the 529 plans. In 2020, you could transfer $75,000 ($150,000 for a married couple) to a 529 plan without generating a gift tax or using up your estate tax exemption.

Fund Health Care Savings Account

If you have a high deductible healthcare plan, consider opening an HSA. If you qualify, you can contribute up to $3,550 for an individual and $7,100 for families, and an additional $1,000 catch-up contribution if you are over 55.

For This Year Only (CARES Act)

- Individuals are not required to take a Required Minimum Distribution from their retirement accounts

- “Coronavirus-related” retirement account withdrawals will not be subject to a 10% early withdrawal penalty. They will still be subject to ordinary income tax, however, the tax can be spread over three years.

- Individuals who do not itemize deductions on their income tax return can deduct up to $300 of cash only contributions to qualifying charities.

- The definition of qualifying educational payments that can be excluded from gross income has been expanded for payments made before January 1, 2021. Subject to a per employee limit of $5,250.

As always, be sure to discuss major life events with your advisor, such as marriages, divorces, births or deaths in the family, job or employment changes and significant upcoming expenses (i.e. real estate purchases, college tuition, etc.) Please feel welcome to contact us with any questions regarding the above-mentioned strategies.

Views expressed areas of date indicated, based on information available at that time, and may change based on market and other conditions. Unless otherwise noted, the opinions provided are those of the Sandy Cove Advisors. Sandy Cove Advisors does not assume any duty to update any of the information. Information provided is general in nature. It is not intended to be, and should not be construed as, legal or tax advice. Sandy Cove Advisors does not provide legal or tax advice. Laws of a specific state or laws relevant to a particular situation may affect the applicability, accuracy, or completeness of this information. Consult an attorney or tax advisor regarding your specific legal or tax situation.Sources: Internal Revenue Service, Fidelity Year-End Tax Strategies, Kiplinger |